PND 51 — Thailand's Half-Year Corporate Income Tax: How to Calculate, When to File, and the 25% Penalty You Must Avoid

Article Content

# PND 51 (ภ.ง.ด.51) — Thailand's Half-Year Corporate Income Tax: How to Calculate, When to File, and the 25% Penalty You Must Avoid

Your company files PND 30 (ภ.พ.30) every month and PND 50 (ภ.ง.ด.50) every year — but did you know there is another form that many companies forget entirely, and then get hit with a 20% surcharge for forgetting? That form is PND 51 (ภ.ง.ด.51).

PND 51 is the mid-year corporate income tax return that most Thai companies must file within 2 months after the end of the 6th month of their accounting period, along with a prepayment of corporate income tax based on estimated profit. If the estimated profit falls more than 25% short of actual profit without reasonable cause, the company will be charged an additional 20% surcharge on the tax shortfall under Section 67 Tri (มาตรา 67 ตรี) of the Revenue Code.

What Is PND 51? Who Must File, and Who Is Exempt?

PND 51 is the mid-year corporate income tax declaration form covering the first half of the accounting period. It is mandated under Section 67 Bis (มาตรา 67 ทวิ) of the Revenue Code to require companies to prepay corporate income tax during the mid-year period, before filing the annual PND 50 (ภ.ง.ด.50) at the end of the accounting period. Whether your business sells through TikTok Shop, Shopee, Lazada, or earns revenue through other channels, if you are registered as a company or juristic partnership you are required to file PND 51.

Juristic persons required to file PND 51:

- Private limited companies (บริษัทจำกัด)

- Public limited companies (บริษัทมหาชนจำกัด)

- Juristic partnerships (ห้างหุ้นส่วนนิติบุคคล)

- Other juristic persons required to file PND 50

With one key condition: the accounting period must be exactly 12 months in length.

Cases exempt from filing PND 51:

- First or final accounting period shorter than 12 months — for example, a company registered on 1 July using a 1 Jan–31 Dec accounting period will have only 6 months in its first period and is therefore exempt.

- Foundations and associations — not required to file PND 51.

- Individuals — PND 51 applies only to juristic persons; individuals use PND 94 (ภ.ง.ด.94) instead.

Important: A newly registered company whose first accounting period is exactly 12 months is NOT exempt — it must file PND 51 the same as any established company.

2 Methods for Calculating Half-Year Tax: Which Applies to Your Business?

General SMEs must always use Method 1 (estimated full-year profit ÷ 2). Method 2 (actual first-half profit) is available only to companies listed on the Stock Exchange of Thailand, banks, and companies given special approval by the Director-General of the Revenue Department, under Section 67 Bis of the Revenue Code.

Method 1 — Estimated Net Profit (for most companies)

Companies must estimate their full-year net profit and calculate tax as follows:

- Estimate full-year net profit

- Divide by 2 to obtain "estimated half-year profit"

- Calculate tax at the applicable rate

- Pay the tax amount calculated

Example: Company A estimates its full-year net profit at THB 1,500,000.

| Item | Amount |

|---|---|

| Estimated full-year net profit | THB 1,500,000 |

| Half-year profit (÷ 2) | THB 750,000 |

| Tax (15% for SME profit between THB 300,001–3,000,000) | THB 112,500 |

| Amount payable under PND 51 | THB 112,500 |

Method 2 — Actual First-Half Profit (for eligible juristic persons only)

Only the following entities may use this method under Section 67 Bis (2) of the Revenue Code:

- Companies listed on the Stock Exchange of Thailand (SET)

- Commercial banks

- Finance companies, securities companies, credit foncier companies

- Life insurance companies

- Juristic persons approved by the Director-General of the Revenue Department to have their interim financial statements audited by a CPA (per Director-General's Announcement on Income Tax No. 128)

This method uses the actual net profit of the first 6 months to compute tax directly, and requires CPA review along with submission of interim financial statements.

Side-by-Side Comparison of Both Methods

| Method 1 — Estimated Profit | Method 2 — Actual Profit | |

|---|---|---|

| Who can use it | All general SMEs | SET-listed, banks, insurers, or specially approved entities |

| Basis of calculation | Estimated full-year profit ÷ 2 | Actual net profit for first 6 months |

| CPA review required | Not required | Yes — interim financial statements must be submitted |

| 25% rule risk | Higher (depends on accuracy of estimate) | Lower (based on actual figures) |

Corporate Income Tax Rates Used for Calculation

| Net Profit | Tax Rate (eligible SMEs) | General Rate |

|---|---|---|

| ≤ THB 300,000 | 0% | — |

| THB 300,001–3,000,000 | 15% | — |

| > THB 3,000,000 | 20% | 20% |

SMEs with paid-up capital not exceeding THB 5 million and annual revenue not exceeding THB 30 million qualify for the reduced rates. Companies that do not meet SME criteria are taxed at a flat 20%.

When Is PND 51 Due, and What Are the Payment Channels?

Filing Deadlines

The law requires PND 51 to be filed within 2 months from the last day of the 6th month of the accounting period, per Section 67 Bis of the Revenue Code.

| Accounting Period | End of First 6 Months | Paper Filing Deadline | e-Filing Deadline |

|---|---|---|---|

| 1 Jan–31 Dec | 30 June | 31 August | 8 September |

| 1 Apr–31 Mar | 30 September | 30 November | 8 December |

| 1 Jul–30 Jun | 31 December | 28 February | 8 March |

Most companies in Thailand use the 1 Jan–31 Dec period. The filing deadline is 31 August (or 8 September for e-Filing).

Online filers through the e-Filing system at rd.go.th receive an 8-day extension — make full use of this benefit.

Payment Channels

- Online filing via the e-Filing system at rd.go.th — pay via e-Payment or Internet Banking in a single step

- Internet Banking through participating commercial banks (Krungthai, KBank, Krungsri, GSB, and others)

- Bank counter with a completed PND 51 form

- Area Revenue Office where the company is located

The 25% Rule: Why It Matters and 2 Ways to Avoid the Penalty

Section 67 Tri — The Penalty Many Companies Overlook

If a company's estimated profit falls more than 25% short of what is declared in PND 50 (actual year-end profit) without "reasonable cause," the Revenue Department will impose an additional 20% surcharge on the tax shortfall under Section 67 Tri (มาตรา 67 ตรี) of the Revenue Code.

Example:

| Item | Amount |

|---|---|

| Estimated profit in PND 51 | THB 500,000 |

| Tax paid under PND 51 | THB 30,000 |

| Actual profit at PND 50 year-end | THB 1,000,000 |

| Tax that should have been paid based on actual profit | THB 105,000 |

| Tax shortfall | THB 75,000 |

| 20% surcharge | THB 15,000 |

Estimated profit THB 500,000 vs actual profit THB 1,000,000 = shortfall of 50% → exceeds 25% → surcharge applies

2 "Safe Harbor" Options Under Revenue Department Order Por. 152/2558

Companies that satisfy at least one of the following two conditions are deemed to have "reasonable cause" — the 20% surcharge will not apply even if the estimate deviates by more than 25%:

Safe Harbor 1: The tax paid under PND 51 is not less than 50% of the corporate income tax paid under the prior year's PND 50.

| Item | Amount |

|---|---|

| Tax paid under prior year PND 50 | THB 100,000 |

| 50% of prior year tax | THB 50,000 |

| Minimum amount payable under PND 51 | ≥ THB 50,000 |

This method works well for businesses with relatively steady revenue who have not yet clearly projected this year's profit.

Safe Harbor 2: The estimated net profit in PND 51 is not less than the net profit of the prior accounting period, regardless of whether the calculated tax is lower than the prior year (for any reason — including cases where no exemptions are currently available).

This option applies to companies whose current-year profit is expected to be close to or higher than the prior year. No special exemption is required to use this safe harbor.

Guidance for New Companies with No Prior-Year Data

Companies that have never filed PND 50 before cannot use either safe harbor option — there is no prior-year baseline.

Common example for Orbit clients: A company registered on 1 January 2026 using a Jan–Dec accounting period has a full 12-month period and must file PND 51 by 31 August 2026 (or 8 September 2026 via e-Filing) with no safe harbor protection. The solution is to estimate profit in a reasonable and honest manner, referencing actual business results from January through June and projecting the second half carefully.

If you are unsure what profit to estimate, we recommend consulting Orbit Advisory before the filing deadline.

Can You File PND 51 with Zero Profit? The Risk Many Companies Miss

Legally, a company may file PND 51 declaring zero estimated profit. There is no direct prohibition.

However, the risks are as follows:

If the company shows a profit at year-end and the actual profit exceeds the estimate (zero) by more than 25% — which, if you estimated zero, means even THB 1 of actual profit triggers the threshold — the company will face the 20% surcharge under Section 67 Tri of the Revenue Code.

Cases where filing zero is genuinely safe:

- The company genuinely incurred a loss for the year with no possibility of turning profitable

- Or the zero tax amount under PND 51 is still at least 50% of the prior year's PND 50 tax (possible only if no tax was paid in the prior year either)

Safer alternative: Even if a loss is expected, consider estimating a conservatively low profit to create a "floor" that protects against the case where actual results turn profitable. Always consult an accounting firm before filing zero.

How Does PND 51 Connect to PND 50? Can You Get a Refund?

Section 68 (มาตรา 68) of the Revenue Code provides that the tax paid under PND 51 serves as a tax credit to be deducted from the tax liability under the annual PND 50.

Possible outcomes:

| Scenario | Result |

|---|---|

| PND 50 tax > tax paid under PND 51 | Pay the balance with PND 50 |

| PND 50 tax = tax paid under PND 51 | No additional payment, no refund |

| PND 50 tax < tax paid under PND 51 | Claim a refund of excess tax, or carry forward as a credit to the next year |

If you over-estimated and paid more tax than required, the company is entitled to apply for a refund, filed together with PND 50. To understand how the net profit used in PND 50 is derived, read 5 Legal Ways Business Owners Can Withdraw Money from Their Company, which covers corporate tax planning in the broader context.

Penalties for Not Filing or Filing PND 51 Late

Many companies are unaware that PND 51 carries its own separate penalties from PND 50, which means they can be penalized on both.

1. Criminal fine (Section 35 of the Revenue Code)

- Fine of up to THB 2,000 for non-filing or late filing

2. Surcharge (Section 27 of the Revenue Code)

- 1.5% per month of the outstanding tax (fractions of a month count as a full month)

- Accrues from the due date until actual payment — no 20% cap — the longer you wait, the more it accumulates

Advantage of self-filing before a Revenue Department summons: If the company files PND 51 voluntarily before the Revenue Department issues an audit notice, the surcharge is only 1.5%/month (Section 27, paragraph 2 of the Revenue Code) — compared to being audited and potentially facing additional assessment penalties.

When the Revenue Department finds that PND 51 was not filed, or that the tax amount deviates significantly from PND 50, an officer will issue a summons requesting an explanation and will assess additional tax plus a penalty of 1–2 times the tax shortfall under Sections 22 and 26 of the Revenue Code.

Comparison: Filing 3 months late → 4.5% surcharge on outstanding tax — still far less than the 20% surcharge for underestimating profit by more than 25%.

5 Common PND 51 Mistakes SMEs Make — and What to Watch For

The following are the 5 most frequent causes of surcharges and penalties from PND 51 — check which apply to your business.

Mistake 1: Forgetting to file entirely

Many companies know only PND 50 and PND 30 and have never heard of PND 51 — either because their accounting firm never alerted them, or because the detail was lost during a change of accountant. This is especially common in companies that have just passed their first accounting period.

Mistake 2: Filing zero without assessing the risk

As discussed above, if the year-end result shows a profit, a company that filed zero will immediately face the 20% surcharge with no safe harbor available.

Mistake 3: Not knowing the "50% safe harbor" under Por. 152/2558

Many companies underpay because they estimate too low, when knowing that paying just 50% of the prior year's tax is sufficient would give them a definitive, safe number to use.

Mistake 4: Calculating the 25% threshold against the prior year instead of this year's actual profit

Many people misunderstand the rule and think "25%" is measured against prior-year performance. In fact, the law compares estimate vs actual profit (PND 50) within the same year. A company whose profit grows much more than expected within the same year — not simply because last year was lower — is where the risk lies.

Mistake 5: Not using e-Filing and losing the 8-day extension

The paper deadline is end of August, but online filing at rd.go.th is available until early September. Companies that rush to file on paper simply because they don't know about this lose valuable time unnecessarily.

Accurate profit calculation is the foundation of safe PND 51 filing — read 10 Non-Deductible Expenses for Corporate Tax Thailand (Section 65 Tri) to ensure the net profit you are using does not include any prohibited expenses.

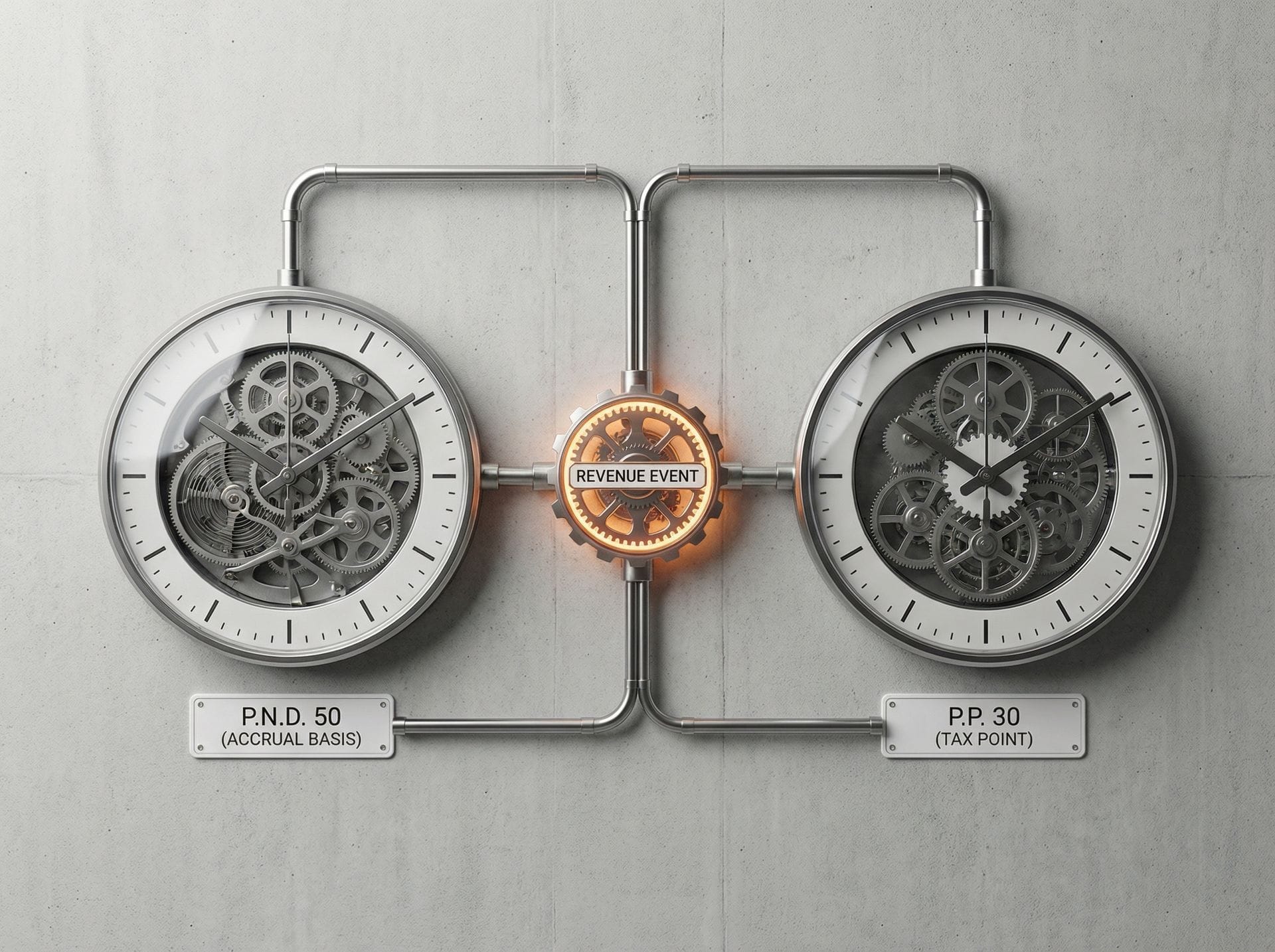

If you also want to understand how net profit under PND 50 differs from VAT, read CIT vs VAT: Accrual Basis vs Tax Point for an explanation of the revenue recognition principles used in corporate income tax.

Summary: How to File PND 51 Safely

PND 51 is not just another tax form — it is the point where many companies get hit with a 20% surcharge without realizing it, either by underestimating profit or forgetting to file entirely.

| Your Situation | Recommended Approach |

|---|---|

| Newly established company, first year, 12-month accounting period | Must file PND 51 — no prior-year baseline; must estimate profit reasonably |

| Company with prior tax history | Use Safe Harbor 1 (50%) — pay at least 50% of prior year's tax; safest option |

| Profit expected to be higher than prior year | Use Safe Harbor 2 — estimate profit no lower than prior year |

| Expected loss | Consult an accountant before filing zero — high risk if result turns profitable |

| Want a professional to handle it completely | Consult Orbit Advisory on corporate tax |

Not sure whether your company needs to file, how to calculate, or which safe harbor to use? Contact Orbit Advisory and let a specialist help you plan your corporate tax correctly from the start.

Frequently Asked Questions About PND 51

Q1: Does a newly registered company need to file PND 51 in its first year?

A: A company whose first accounting period is exactly 12 months must file PND 51 as normal. If the first accounting period is shorter than 12 months (e.g., registered mid-year), it is exempt from filing for that period under Section 67 Bis (มาตรา 67 ทวิ) of the Revenue Code. In summary: the rule is based on the actual length of the accounting period, not whether the company is new or established.

Q2: Can a company file PND 51 with zero estimated profit if it expects a loss this year?

A: Filing with zero is legally permitted, but it carries risk. If the actual year-end result turns profitable, and that profit exceeds the zero estimate by more than 25%, the company will face a 20% surcharge under Section 67 Tri (มาตรา 67 ตรี) of the Revenue Code. We recommend consulting an accountant before deciding to file zero, especially if there is any possibility of profit in the second half of the year.

Q3: When is the PND 51 filing deadline?

A: For companies using a 1 January–31 December accounting period (the most common in Thailand), the deadline is 31 August for paper filing and 8 September for online filing via e-Filing at rd.go.th, per Section 67 Bis of the Revenue Code and the Director-General's announcement extending the e-Filing period by 8 days.

Q4: How much is the surcharge if PND 51 profit is underestimated by more than 25%?

A: A 20% surcharge on the tax shortfall is imposed, under Section 67 Tri (มาตรา 67 ตรี) of the Revenue Code. For example, if the tax shortfall is THB 50,000, the surcharge is THB 10,000. This can be avoided by using the safe harbor options under Order Por. 152/2558 — paying at least 50% of prior year corporate income tax, or estimating profit no lower than prior year profit.

Q5: Can PND 51 be filed online, and how does it differ from paper filing?

A: PND 51 can be filed online via the e-Filing system at rd.go.th. The key difference is the deadline — online filers receive an 8-day extension (e.g., a January–December company can file until 8 September instead of 31 August). Online filing also allows immediate payment via Internet Banking in a single step, making it more convenient and reducing the risk of late submission.

📚 Related Articles

10 Prohibited Expenses (Section 65 Tri) That Companies Most Often Get Wrong on Their Corporate Tax Return

Section 65 Tri prohibited expenses: the 10 most common mistakes Thai SMEs make on their corporate income tax return and how to fix them before filing.

How Can Business Owners Withdraw Money from Their Company? 5 Legal and Tax-Efficient Methods Revealed

5 legal ways for Thai business owners to withdraw money from their company — with tax rates and compliance requirements for each method explained.

CIT vs VAT: Understanding Accrual Basis vs Tax Point - Critical Guide for Thai Business Owners

Corporate income tax uses accrual basis; VAT uses the tax point. Confusing them causes mismatches in ภ.ง.ด.50 vs ภ.พ.30 filings — this guide clarifies both.

Swipe to see more →

Ready to Take Action?

Our expert team is ready to help you achieve your financial goals. Contact us through your preferred channel.