How Can Business Owners Withdraw Money from Their Company? 5 Legal and Tax-Efficient Methods Revealed

Article Content

How Can Business Owners Withdraw Money from Their Company? 5 Legal and Tax-Efficient Methods Revealed

One of the most common questions SME business owners ask is: "How can I legally withdraw money earned from my company for personal use?" Many business owners may inadvertently mix company funds with personal money, which creates significant tax risks. The Revenue Department may assess retroactive taxes with penalties and surcharges.

This article by Orbit Advisory explores 5 legal methods for withdrawing money from your company in compliance with Revenue Department regulations. We'll analyze the tax implications of each method so you can plan effectively and safely as a business owner.

1. Salary and Director Remuneration

This is the most basic and straightforward method: paying directors as "employees" or "executives" of the company.

Legal Principles and Conditions

For director salaries to be deductible as company expenses under Section 65(13) of the Revenue Code, they must be "reasonable" and comply with conditions specified in shareholder meeting resolutions or company articles of association.

Key Conditions:

- Must be specified in Articles of Association: Company articles must authorize shareholder meetings to determine director remuneration.

- Must have meeting resolution: Director salary or remuneration rates must be approved in shareholder meetings.

- Must be reasonable: Salary rates must be reasonable relative to responsibilities, workload, and company performance. Not excessively high compared to similar businesses in the same industry.

Implementation Steps

- Prepare shareholder meeting documents to approve remuneration framework or rates for directors.

- Company pays directors monthly salaries.

- Company must withhold Withholding Tax at progressive rates and file Form PND.1 by the 7th of the following month.

- Company must register as employer and submit social security contributions for directors (as employees).

Example

Company A has net profit before director salaries of 5,000,000 THB and wants to pay director Mr. B a monthly salary of 100,000 THB (1,200,000 THB annually).

- Company side: Can deduct 1,200,000 THB as expenses, reducing taxable profit to 3,800,000 THB, saving 240,000 THB in corporate income tax (1,200,000 x 20%).

- Director side: Mr. B has assessable income of 1,200,000 THB, which must be included in personal income tax calculation at year-end, taxed at progressive rates.

Advantages

✅ Company expense: Reduces net profit, lowering corporate income tax. ✅ Builds credibility: Shows company has systematic management structure. ✅ Employee benefits: Directors receive company employee welfare benefits.

Disadvantages and Risks

⚠️ High personal tax burden: Salaries taxed at progressive rates (need to plan director's personal deductions). ⚠️ Must submit social security: Incurs costs and monthly contribution obligations. ⚠️ Risk if unreasonable: If Revenue Department deems salary excessive, may disallow as company expense, resulting in additional corporate tax plus penalties and surcharges.

2. Dividends

Dividends are distribution of company accumulated profits back to shareholders, best reflecting business performance.

Legal Principles and Conditions

Dividend payments must comply with Civil and Commercial Code and Revenue Code.

- Must be paid from profits: Companies can only pay dividends when they have accumulated profits and have set aside legal reserves (at least 10% of registered capital).

- Corporate tax paid first: Dividends are paid "after" company has already paid 20% corporate income tax.

Implementation Steps

- Board of Directors meeting to resolve to pay dividends.

- Shareholders meeting to approve dividend payment.

- Announce dividend payment to shareholders.

- When paying dividends, company must withhold 10% withholding tax and file Form PND.2 (when paying to individuals).

Example

Company A has Mr. B as 100% shareholder with the following profit status:

Year 1 Status • Annual net profit: 20,000 THB • Accumulated profits brought forward: 0 THB • Year-end accumulated profits (unappropriated): 20,000 THB • Dividend payment: None • Legal reserve requirement: Since no dividends paid, company has no legal reserve obligation in Year 1 • Unappropriated retained earnings carried to Year 2: 20,000 THB

Year 2 Status (wanting to pay dividends)

- Calculate distributable accumulated profits

• Accumulated profits from Year 1: 20,000 THB • Net loss for Year 2: (5,000) THB • Remaining accumulated profits at Year 2 end (before dividend payment): 20,000 - 5,000 = 15,000 THB

Since company still has remaining accumulated profits (not accumulated deficit), company can pay dividends under Section 1201.

- Calculate legal reserve

• Principle: Must set aside 5% of "profits" each time dividends are paid • "Profits" here means the profit base used for dividend payment, which comes from Year 1 profits of 20,000 THB (even though reduced by Year 2 losses) • Legal reserve calculation: 5% x 20,000 THB = 1,000 THB

- Calculate maximum dividend payable

• Distributable accumulated profits: 15,000 THB • Less: Required legal reserve: (1,000) THB • Maximum dividend payable: 15,000 - 1,000 = 14,000 THB

- Company A side:

Shareholders meeting can approve allocation of 15,000 THB accumulated profits as follows: • Allocated as legal reserve: 1,000 THB • Allocated for dividend payment: 14,000 THB Must withhold 10% tax at source amounting to 1,400 THB (14,000 x 10%)

- Director (shareholder) side: Mr. B will receive 12,600 THB cash and has 2 tax options:

- Final Tax: Accept 10% withholding as final, no need to include in year-end tax calculation.

- Dividend tax credit: Include 12,600 THB dividend with other income in tax calculation, worthwhile if personal tax base is low and taxed at rate below 10%.

Advantages

✅ Lower personal tax possible: If choosing Final Tax, taxed at flat 10% rate, often lower than highest salary tax rate. ✅ Flexible: Can choose to pay in years when company has high liquidity.

Disadvantages and Risks

⚠️ Not company expense: Dividends paid from after-tax profits, cannot deduct as expense to reduce corporate tax. ⚠️ Double taxation: Same money taxed twice (20% corporate tax at company level, 10% withholding at shareholder level). ⚠️ Complex process: Requires multiple legal meeting steps and documentation.

3. Loans to Directors

Method where company lends money to directors for personal use, with clear repayment terms and conditions.

Legal Principles and Conditions

Key focus for Revenue Department is "interest rate"

- Must charge interest: Company must charge directors interest at "market rate". If no interest charged or below market rate, Revenue Department will assess imputed interest income for company, and treat uncharged interest as director income too.

• If using company's own funds: Safe practice is using "bank deposit interest rate" at that time as reference benchmark. • If company borrowed from bank to lend to director: Must charge interest "not lower than" rate company pays to that lender, to avoid being deemed having fake expenses or profit transfer.

- Must have clear agreement: Must have loan agreement specifying amount, interest rate, and clear repayment schedule.

Implementation Steps

- Prepare loan agreement between company (lender) and director (borrower).

- Company pays loan amount to director.

- Director must repay principal plus interest per agreement.

- Company must recognize interest income and include in corporate tax calculation.

- Interest company receives from director (individual) not subject to withholding tax, but company must issue tax invoice and pay VAT if company is VAT registered and lending constitutes business activity.

Advantages

✅ Short-term liquidity: Quick method to withdraw money for personal use in short term. ✅ No immediate tax: Principal loaned not considered director's income.

Disadvantages and Risks

⚠️ Must repay: It's debt, not income. Director obligated to repay company. ⚠️ High tax risk: If no interest charged or no strict agreement, Revenue Department can assess retroactive tax on both company and director. ⚠️ May impact company liquidity: Large loans may drain company working capital.

4. Rental Fees

Case where director owns assets (e.g., office building, car) and company rents those assets from director for business use.

Legal Principles and Conditions

Like salaries, rental fees must be at "reasonable" rates or market prices to be deductible as company expenses.

Implementation Steps

- Prepare rental agreement between director (lessor) and company (lessee).

- Company pays rental fees to director per agreement.

- Company must withhold 5% withholding tax for immovable property rental and file Form PND.3.

- Director includes rental income in personal income tax calculation, can deduct 30% flat expense or actual expenses.

Advantages

✅ Company expense: Rental fees deductible as company expenses. ✅ Creates personal income for director: Generates regular cash flow for director.

Disadvantages and Risks

⚠️ Must be director's actual asset: Must have clear proof of asset ownership. ⚠️ Risk if rental excessive: If rental above market rate, Revenue Department may disallow excess portion.

5. Interest Income

Reverse of case #3, where director lends to company and company pays interest back to director.

Legal Principles and Conditions

Interest rate company pays director must be reasonable at market rates to be deductible as company expense.

Implementation Steps

- Prepare loan agreement between director (lender) and company (borrower).

- Company pays interest to director per agreement.

- Company must withhold 15% withholding tax for interest and file Form PND.2.

- Director can choose to make 15% tax Final Tax or include in year-end tax calculation.

Advantages

✅ Company expense: Interest paid is tax-deductible expense. ✅ Low personal tax: If choosing Final Tax, taxed at flat 15% rate.

Disadvantages and Risks

⚠️ Must have actual lending: Must have proof of money transfer from director to company. ⚠️ Must have appropriate interest rate: If too high, may be deemed profit transfer.

Comparison Table: 5 Methods to Withdraw Money from Company

| Method | Company Tax Side | Director/Shareholder Tax Side | Biggest Advantage | Biggest Caution |

|---|---|---|---|---|

| 1. Salary/Remuneration | Deductible expense (saves 20% tax) | Progressive tax (5-35%) | Directly reduces corporate tax | High personal tax burden, must be reasonable |

| 2. Dividends | Not deductible (paid from after-tax profits) | 10% withholding (can choose Final Tax) | Personal tax side may be lower | Double taxation occurs |

| 3. Loans to Directors | Interest income taxed 20% | Principal not taxed, but uncharged interest deemed income | Short-term liquidity | ⚠️ HIGHEST RISK if no market-rate interest charged |

| 4. Rental Fees | Deductible expense (saves 20% tax) | 5% withholding, included in year-end tax | Creates regular director income, company expense | Rental rates must follow market prices |

| 5. Interest (director lends) | Deductible expense (saves 20% tax) | 15% withholding (can choose Final Tax) | Company expense, personal side can be Final Tax | Must have actual lending transaction occur |

Warnings and Risks of Improper Withdrawals

Withdrawing money from company without proper documentation, such as cash withdrawals for personal use without supporting documents, Revenue Department may view this in several ways, all unfavorable:

- Deemed director loan: But no interest charged, will assess interest income and related taxes.

- Deemed remuneration/bonus payment: Will be included as director income, and company may be disallowed from deducting as expense without proper meeting resolution.

- Consequences: Retroactive tax assessment, penalties up to 2x tax amount, and surcharge additional 1.5% per month on payable tax.

Summary

No single method is best. Choosing appropriate withdrawal method depends on shareholder structure, director's personal tax burden, company performance, and company liquidity. Best planning often uses multiple methods combined, such as setting reasonable salary levels and paying dividends in high-profit years.

Given tax planning complexity in this area directly affecting both company and you personally, consulting experts to structure appropriately for your specific business is essential.

If you need in-depth consultation to plan tax for directors and shareholders to maximize benefits, contact Orbit Advisory experts immediately

Frequently Asked Questions (FAQ)

Q1: Which method saves the most tax? A: Depends on situation. If director's personal tax base is high (e.g., 30-35%), receiving dividends with 10% Final Tax may be better. But if tax base is low, receiving salary for company to deduct as expense may be better overall. Should consider case-by-case.

Q2: Can I set very high director salaries to make company show small profits? A: Not recommended. Revenue Department has authority to assess whether salaries are "reasonable." If excessive compared to responsibilities and performance, may disallow excess portion as deductible expense.

Q3: If company has losses, can dividends still be paid? A: No. Legal dividend payments must come from "profits" only. However, company can still pay "salaries" to directors normally even in loss years.

Q4: Can company borrow money without charging any interest? A: No. Per Revenue Department principles, if money is lent, must charge market-rate interest. If no interest charged, company deemed to have taxable income, and director received benefit subject to tax too.

Q5: Can directors expense all personal costs like fuel, meals from company? A: No. Expenses claimable from company must be "directly related to company operations" with supporting evidence. Taking personal expenses as company expenses creates significant tax risk.

📚 Related Articles

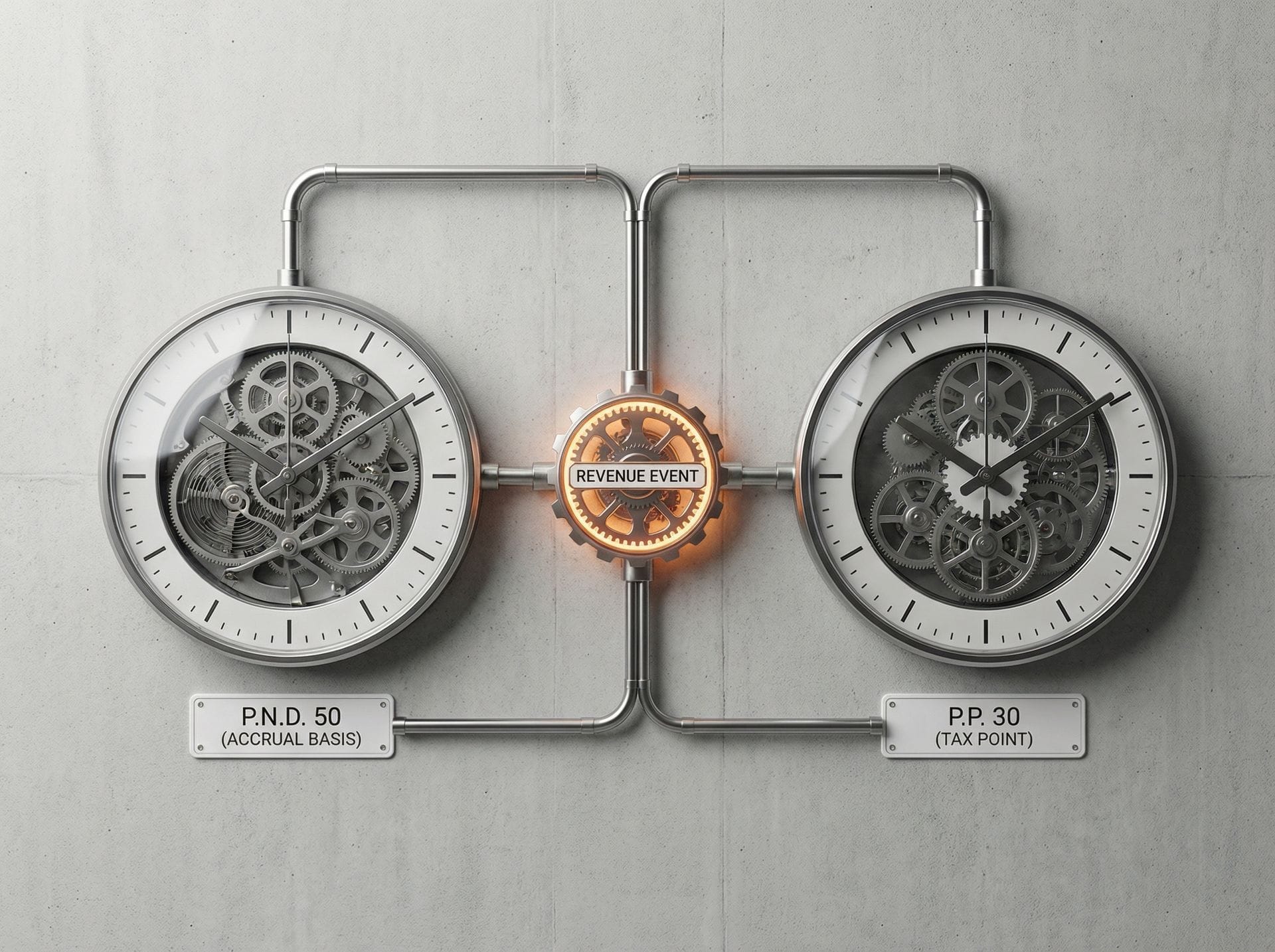

CIT vs VAT: Understanding Accrual Basis vs Tax Point - Critical Guide for Thai Business Owners

Corporate income tax uses accrual basis; VAT uses the tax point. Confusing them causes mismatches in ภ.ง.ด.50 vs ภ.พ.30 filings — this guide clarifies both.

Deep Dive into 8 Types of Income (40(1) – 40(8)): What Type is Your Income and How to Deduct Expenses for Maximum Tax Savings?

Thailand's Revenue Code classifies income into 8 types (Section 40). Your type determines deduction rates — the difference can be tens of thousands of baht.

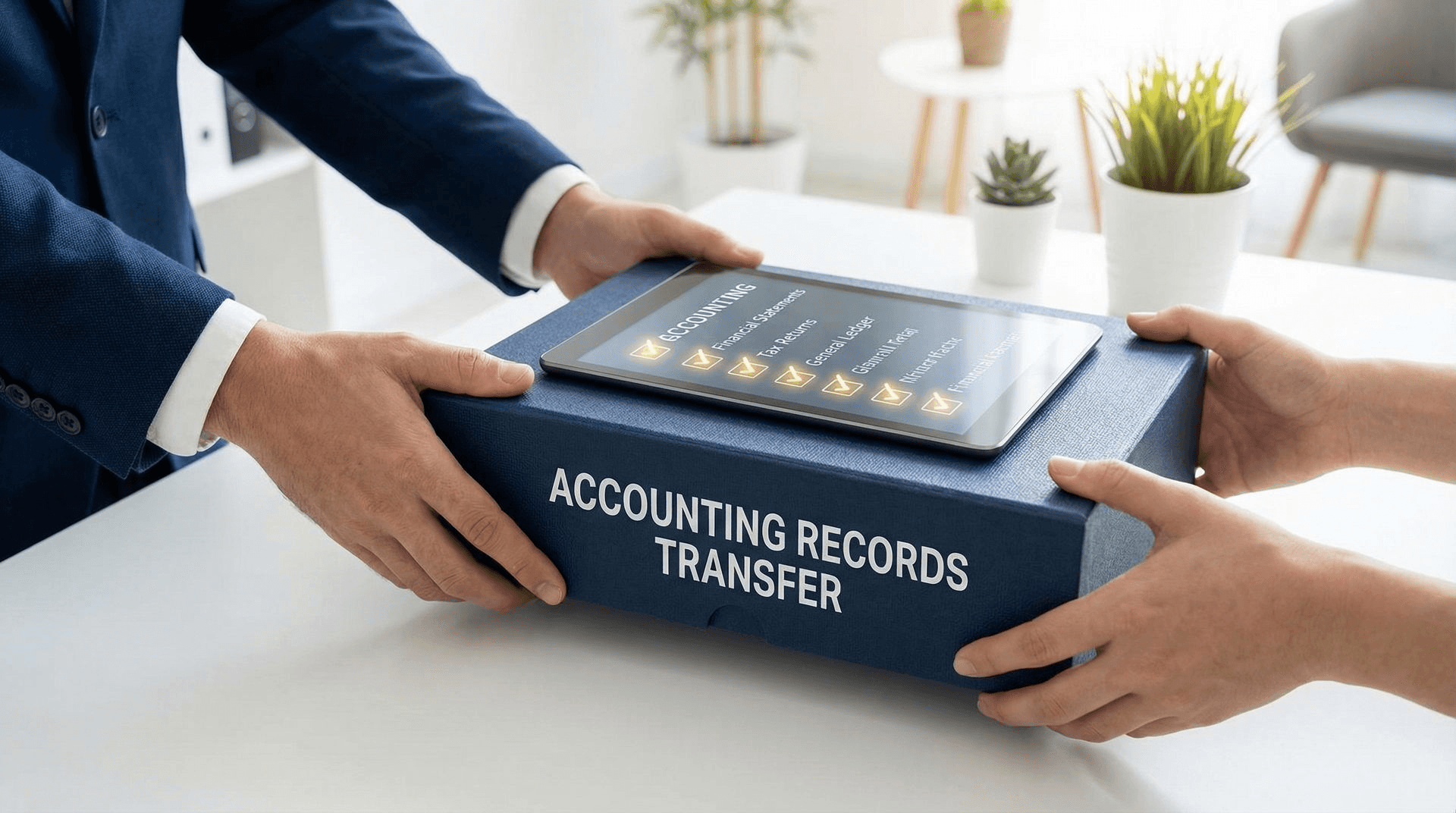

Changing Accounting Firms Mid-Year: Big Deal or Easy Task? (With Document Handover Checklist)

Switching accounting firms mid-year is straightforward if done right. This checklist covers documents to reclaim, handover steps, and tax-filing continuity.

Swipe to see more →

Ready to Take Action?

Our expert team is ready to help you achieve your financial goals. Contact us through your preferred channel.