Why Financial Statements Must Be Audited and Certified by Certified Public Accountants

Article Content

Why Financial Statements Must Be Audited and Certified by Certified Public Accountants

For SME business owners without an accounting background, you may wonder why legal entities like companies or partnerships must prepare financial statements every year and have them audited and certified by Certified Public Accountants (CPAs). This article will explain the reasons in straightforward terms to give you a clear picture of how necessary financial statement audits are, both legally and from a business perspective.

Thai Legal Requirements and Penalties

Thai law requires legal entities to prepare financial statements annually. Registered companies and partnerships have the obligation to prepare and submit financial statements to the Department of Business Development (DBD) (commonly referred to as "submitting financial statements to the DBD") and submit income tax returns along with financial statements to the Revenue Department within the specified deadlines each year. Businesses must close their financial statements and proceed as follows:

- Submit financial statements to the DBD: Within one month after financial statements are approved by the shareholders' meeting or within 5 months from the accounting period end date For example, financial statements for the year ending December 31 must be submitted to the DBD by May 31 of the following year.

- Submit financial statements with PND.50 to the Revenue Department: Within 150 days after the accounting period ends (approximately 5 months), which aligns with the DBD submission deadline.

Financial statements submitted to government agencies must be audited and certified by Certified Public Accountants (CPAs) according to Article 11 of the Accounting Act B.E. 2543. This means financial statements must have the signature and opinion from a CPA stating they "are correct according to standards and accurately reflect the financial condition of the business" before being submitted to government agencies (however, there are exceptions for small registered partnerships in some cases, which will be explained in the summary table below).

Note: Certified Public Accountants (CPAs) are professional accountants who have passed examinations and received licenses from the Federation of Accounting Professions, allowing them to audit and certify financial statements according to law. This differs from "accountants" (company accountants or general accounting offices) in that CPAs have the authority to certify financial statements for legal submission.

The penalties for non-compliance with the law are equally strict:

- Failure to prepare or submit financial statements within the specified time – fines up to 50,000 baht for both the legal entity and responsible directors, with possible additional daily fines until complete submission is made.

- Failure to have financial statements audited by a CPA – in cases of violation (such as submitting unaudited financial statements), fines up to 20,000 baht.

- If multiple years of financial statement submissions are neglected, the DBD may pursue legal action or place the company on a blacklist, preventing any company registration changes until all outstanding financial statements are cleared. Additionally, failure to submit financial statements affects income tax return filing, resulting in tax penalties (such as late PND.50 submission fines up to 2,000 baht and surcharges for overdue tax payments).

In summary: Law mandates that businesses must close and audit financial statements annually for submission to government agencies. Failure to comply results in fines and penalties, both for ensuring accurate financial information and for the benefit of all stakeholders.

Importance of Financial Statements for SMEs

Beyond legal requirements, properly audited financial statements hold significant importance for SME businesses from multiple perspectives:

- Bank Loan Applications: Financial statements are the first documents banks use to evaluate loan approvals for SME businesses. Financial statements clearly reflect operational performance and financial health. If financial statements show consistent profits and strong financial position, this increases the bank's confidence and makes loan approval easier (and may result in better interest rates due to lower risk).

- License Applications and Government Agency Transactions: In many cases, applying for business licenses, government project bids, or requesting benefits from government agencies requires showing historical financial statements to prove business stability and credibility. Examples include Board of Investment (BOI) promotion applications or factory licenses. If financial statements are incorrect or delayed, these processes may be hindered or delayed.

- Business Valuation and Attracting Investors: Financial statements are like a business's report card. Investors or new shareholders looking to join the business typically want to see several years of historical financial statements to analyze growth trends, profitability, and financial position. Audited financial statements create credibility with investors that "the numbers are accurate and trustworthy," which facilitates business negotiations.

- Credibility with Suppliers and Customers: SME businesses with accurate, transparent financial statements certified by CPAs appear more credible to suppliers and customers. This demonstrates having an orderly, transparent, and verifiable financial system, which may affect opportunities with major suppliers or new market expansions.

- Tax Planning and Internal Management: Financial statements are tools that summarize the business's financial picture each year. Management can use financial statement data to analyze financial strengths and weaknesses, plan business growth, and optimize tax planning. For example, if this year's financial statements show high profits, they might plan increased investments or utilize tax benefits to reduce taxes in the following year. Proper financial statements ensure correct tax planning according to law and reduce the risk of tax audits.

Summary: Financial statements are not just about "complying with legal requirements." They offer multiple business benefits in financing, marketing, and risk management. Having properly audited financial statements is like having a "certificate of quality" for your business that opens new opportunities and builds long-term stability.

Summary Table: Business Types vs. Financial Statement Audit Requirements

For easier understanding, here's a summary of financial statement submission and audit requirements for major business types in Thailand:

| Business Type | Annual Financial Statement Submission | CPA Financial Statement Audit |

|---|---|---|

| Sole Proprietorship (single business owner, unregistered general partnership) | ❌ No financial statement submission to DBD required (Only submit personal income tax returns to the Revenue Department annually) | ❌ No CPA audit required (No legal financial statements - use internal accounting reports for tax purposes) |

| Registered Partnership (registered general partnership, or Ordinary Partnership) | ✅ Must prepare and submit financial statements annually within 5 months from accounting period end date (e.g., year-end December 31 statements must be submitted by May 31 of following year) | 🔸 Financial statement audit required - Small partnerships (capital ≤ 5 million baht, assets ≤ 30 million baht, income ≤ 30 million baht) can use Tax Auditors (TA) to audit statements (not necessarily CPAs) - If exceeding these thresholds, must have CPA audit and certify statements according to law |

| Limited Company (private limited companies not listed on stock exchange) | ✅ Must prepare and submit financial statements annually within 5 months after accounting period end date (shareholders' meeting must approve statements within 4 months, and submit to DBD within 1 month thereafter) | ✅ Must have CPA audit and certify financial statements annually (mandatory under the Accounting Act) |

| Public Company Limited (companies listed on Stock Exchange of Thailand) | ✅ Must prepare and submit financial statements annually according to the Public Company Act and securities laws. Public companies must submit annual statements, and if listed on the stock exchange, must also prepare quarterly financial statements | ✅ Must have CPA audit and certify financial statements as well, and for listed companies, auditors must be licensed by the Securities and Exchange Commission (SEC) and must rotate auditors every 5 years according to regulatory requirements |

(Note: Other business types such as foundations, associations, and cooperatives also have obligations to prepare and submit annual financial statements to government agencies and must be audited by Certified Public Accountants according to laws governing each type)

We hope this article helps SME business owners better understand why having financial statements audited by Certified Public Accountants is essential, both from legal compliance requirements and from the business benefits gained from credible financial statements. Remember that good financial statements are like business compasses and risk shields. Therefore, business owners should prioritize annual financial statement closing and auditing for sustainable business growth and stability.

Frequently Asked Questions

Q1: Which types of businesses must prepare and audit financial statements?

A: Generally, all businesses registered as legal entities of any type must prepare annual financial statements and have them audited by accountants. This includes limited companies, public companies, registered partnerships (both ordinary and limited), as well as other registered business forms like foundations and associations, which also have this obligation. Exceptions are businesses operating as sole proprietors (single owners or unregistered partnerships that are not legal entities), which do not need to submit financial statements to the DBD or have CPA audits according to law.

Q2: When must financial statements be closed and audited?

A: This must be done annually after the business's accounting period ends (typically the accounting period is January 1 – December 31, unless some businesses choose different accounting periods). When the accounting period end date arrives, accountants will close the accounting books to prepare financial statements. These are then sent to Certified Public Accountants (CPAs) to verify accuracy and provide certification. This entire process should be completed in the early part of the following year because the law sets financial statement submission deadlines around late May (5 months after year-end). Therefore, the financial statement audit process typically occurs in the first quarter of the following year.

Q3: Do new businesses or businesses without income still need financial statement audits?

A: Yes, you must. Regardless of how small the business is or whether it has income, every company/partnership that is a legal entity must prepare financial statements at year-end, even if it's a zero-income statement (empty statements), and must submit them to the DBD. For newly registered businesses that started operations within the year, they must close statements according to normal year-end procedures (although if registered late in the year, they might request permission to extend the accounting period to cover the following year as well, depending on the case). In summary, even if the business has no profits or hasn't started selling, it must submit audited financial statements according to law every year to show business movement or status.

Q4: What happens if financial statements are not audited or not submitted at all?

A: As explained in the earlier section, there will be fines from both the DBD and Revenue Department. The DBD can fine companies up to 50,000 baht and directors up to 50,000 baht for failure to submit financial statements on time. Additionally, there may be daily fines and the company may be blacklisted, preventing other registration activities (such as director changes, capital increases, business dissolution, etc.) until statements are properly submitted. The Revenue Department will also impose fines under tax law if financial statements are not attached to PND.50 forms or are submitted late. It can be said that failure to submit statements results in losses on all fronts - losing money to fines, damaging business reputation, and losing credibility with suppliers and financial institutions.

Q5: Who are Certified Public Accountants (CPAs) and how do they differ from general accountants?

A: CPAs (Certified Public Accountants) are professional accounting qualifications legally licensed. To become a CPA, one must pass examinations set by the Federation of Accounting Professions and meet specified experience requirements, thus receiving CPA licensure. A CPA's role is to examine the accuracy of business financial statements (prepared by company accountants or bookkeepers) by reviewing supporting documents, various accounting entries, and verifying that statements reflect the true business condition. When examination is complete, the CPA issues an auditor's report with their opinion on the financial statements. If everything is correct according to principles, they will certify that "the financial statements are correct and credible." This report must be attached to financial statements submitted to the DBD and shareholders. Simply put, accountants are responsible for preparing accounting records and financial statements, while auditors (CPAs) are responsible for verifying the accuracy of those statements to create credibility for the financial statements.

📚 Related Articles

Changing Accounting Firms Mid-Year: Big Deal or Easy Task? (With Document Handover Checklist)

Switching accounting firms mid-year is straightforward if done right. This checklist covers documents to reclaim, handover steps, and tax-filing continuity.

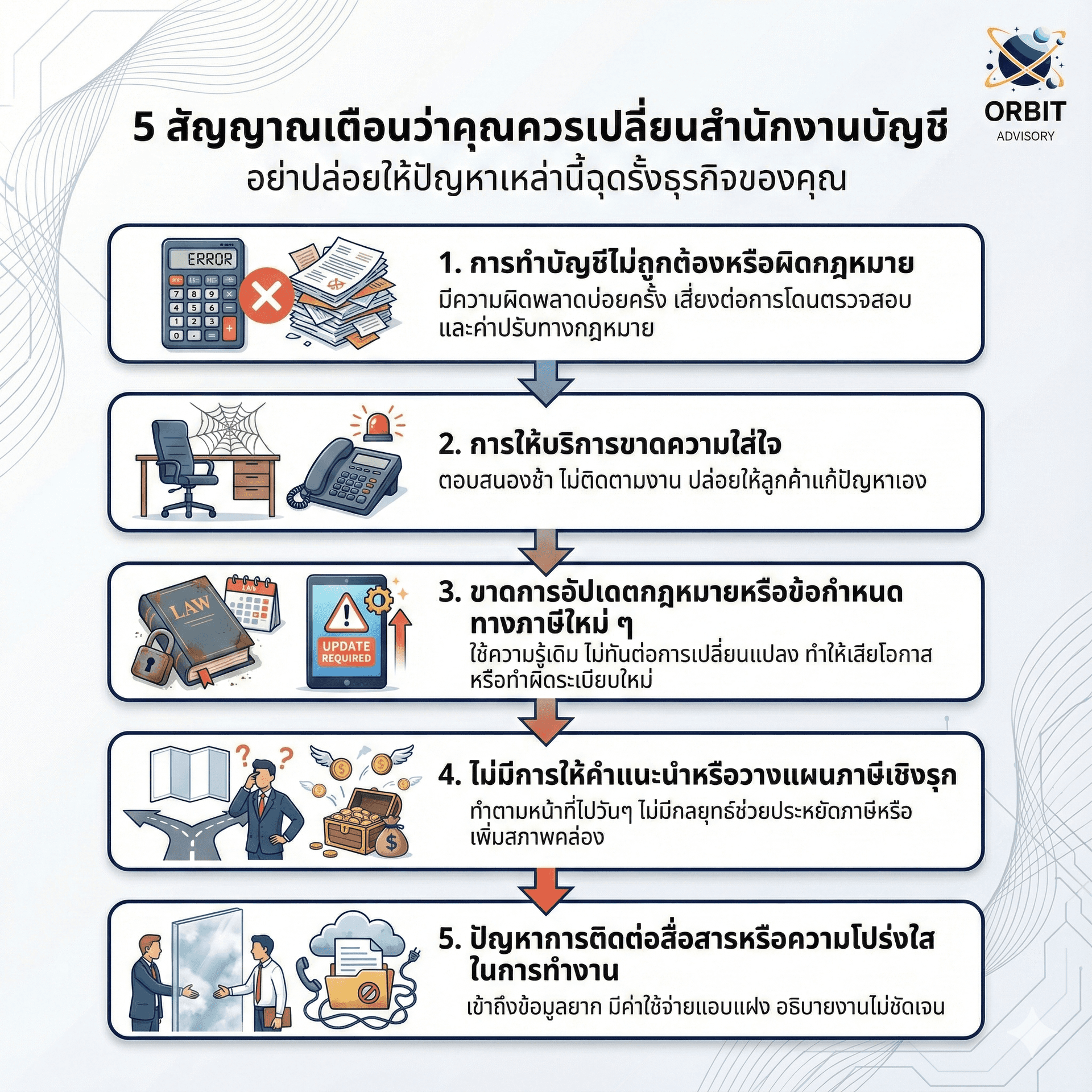

5 Warning Signs You Should Change Your Accounting Firm (Before Facing Retroactive Taxes)

5 red flags that signal your accounting firm is putting your business at risk — and how to switch before the Revenue Department finds problems first.

Document Retention Requirements: Essential Guide to Accounting and Tax Compliance in Thailand

How long must Thai businesses keep accounting and tax documents? Minimum 5 years by law — this guide breaks down what to keep and why.

Swipe to see more →

Ready to Take Action?

Our expert team is ready to help you achieve your financial goals. Contact us through your preferred channel.