Withholding Tax on TikTok Shop and Shopee: Who Must Withhold, What Rate, and Can You Get a Refund?

Article Content

Withholding Tax on TikTok Shop and Shopee: Who Must Withhold, What Rate, and Can You Get a Refund?

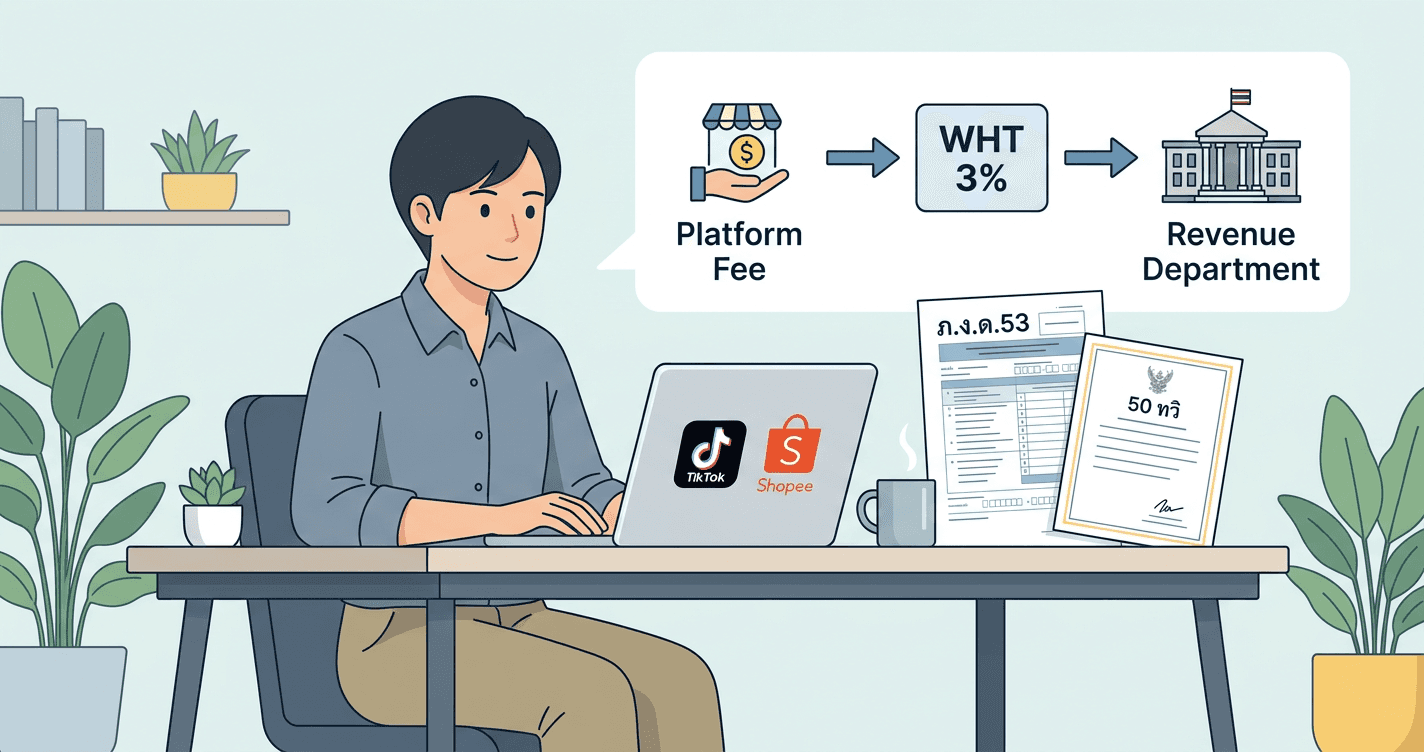

Withholding tax (WHT) for sellers on TikTok Shop and Shopee requires corporate entities to withhold 3% from platform fees and 1% from logistics fees before remitting payment to the platform. Both TikTok Shop and Shopee offer an agent withholding system to handle this automatically. Individual sellers have no withholding obligation in this case.

Have you ever looked at a statement from Shopee or TikTok Shop and noticed a "withholding tax" figure that left you puzzled?

Many sellers mistakenly believe the platform is deducting a "special charge" from their sales revenue — while others have no idea what their tax obligations even are. This article explains it clearly: who must do what, at which rate, what documents are required, and how to handle situations where too much has been withheld.

What Is Withholding Tax, and Why Do Online Sellers Need to Know?

Withholding tax is a mechanism under Thai law that requires the "payer" to deduct a portion of tax before transferring money to the "payee," and remit that withheld amount to the Revenue Department on the payee's behalf. This allows the government to collect tax immediately rather than waiting for the recipient to file at year-end. The mechanism is mandated under Section 3 Tredecim of the Revenue Code and rates are prescribed by Revenue Department Order TP 4/1985.

Online sellers need to understand this because when a business registers as a juristic entity (corporation) and pays fees to platforms such as TikTok Shop or Shopee, that business becomes the "payer" with a legal obligation to withhold tax.

| Legal Reference | Content |

|---|---|

| Section 3 Tredecim of the Revenue Code | Authorizes the Director-General to require payers to withhold tax before payment |

| Revenue Department Order TP 4/1985, Clause 12/1 | Sets the 3% WHT rate on service fees paid to juristic person recipients |

| Revenue Department Order TP 4/1985 | Sets the 1% WHT rate on logistics fees |

| Section 50 Bis of the Revenue Code | Requires the payer to issue a WHT certificate (Form 50 Bis) to the payee |

How Do Obligations Differ Between Individual and Corporate Sellers?

The short answer: individual sellers have no obligation to withhold tax on platform fees, but they must still report their sales income in their annual personal income tax return. Corporate entities have a much more clearly defined obligation.

| Topic | Individual Seller | Corporate Entity |

|---|---|---|

| WHT obligation on platform fees | ❌ None | ✅ Required (3% on service fees, 1% on logistics) |

| Report sales income | ✅ Via Form PND90 at year-end | ✅ Via Form PND50 within 150 days after fiscal year-end |

| Can use platform agent system | ❌ Not applicable | ✅ Recommended |

| WHT filing form | None required | Form PND53 (monthly) |

If you are an individual seller on TikTok Shop or Shopee, your income is classified as assessable income under Section 40(8) of the Revenue Code and must be included in your annual PND90 return filed by March of the following year. You may deduct expenses at a flat rate of 60%. For more details on personal income tax filing for online sellers, see our Online Seller & Influencer Income Tax Guide.

What Platform Fees Must Corporate Entities Withhold Tax On?

For businesses registered as limited companies or registered partnerships, there are two categories of fees that require WHT deduction each time payment is made to the platform: platform fees/commission (3%) and logistics fees (1%).

| Fee Type | WHT Rate | Example |

|---|---|---|

| Platform fee / GP fee / Commission | 3% | GP fee charged by TikTok Shop or Shopee |

| Logistics / Shipping fee | 1% | Shipping via SPX Express (Shopee) or Thai Happy Logistics (TikTok) |

Worked Example: Khun Ton's Case

Khun Ton has a registered company selling cosmetics on TikTok Shop. In February, TikTok Shop charged a platform fee of THB 5,000 (excluding VAT) and a logistics fee of THB 2,000.

WHT that Khun Ton must calculate and remit:

| Line Item | Amount | WHT Rate | Tax to Withhold | Amount Actually Paid |

|---|---|---|---|---|

| Platform fee | THB 5,000 | 3% | THB 150 | THB 4,850 |

| Logistics fee | THB 2,000 | 1% | THB 20 | THB 1,980 |

| Total | THB 7,000 | THB 170 | THB 6,830 |

Khun Ton must remit the THB 170 to the Revenue Department via Form PND53 by the 7th of the following month (or the 15th if filing online), and must issue Form 50 Bis to TikTok Shop as evidence.

💡 However, if Khun Ton has already registered under TikTok Shop's agent system, the platform handles all of these steps automatically.

How Does the "WHT Agent" System Work on Shopee and TikTok Shop?

Both Shopee and TikTok Shop allow corporate sellers to appoint the platform as their "WHT agent." This means the platform will file Form PND53 and remit tax to the Revenue Department on the seller's behalf every month — the seller no longer needs to handle this manually.

Shopee — How to Register for the Agent System

- Log in to Shopee Seller Center → Tax section

- Complete an e-Power of Attorney (electronic authorization) through Shopee's system

- Pay stamp duty via the Revenue Department's e-Stamp Duty system

- Once registered, Shopee and SPX Express will withhold and remit tax on the seller's behalf each month

TikTok Shop — Agent Structure

TikTok Shop uses two separate agent companies depending on the fee type:

| Agent Company | Covers | Rate |

|---|---|---|

| TikTok Shop (Thailand) Ltd. | Platform fee / GP fee | 3% |

| Thai Happy Logistics Ltd. | Logistics fee | 1% |

Sellers can view their agent authorization letters at: Seller Center → Finance → Tax Documents → Authorization Letter

⚠️ Important: If a seller does not register with the agent system, the seller must withhold and remit tax manually every month, including issuing Form 50 Bis to the platform. If you are unsure what needs to be set up, or want a specialist to manage your monthly PND53 filings, the Orbit Advisory team is ready to help.

What Is Form 50 Bis in the Context of Platform WHT, and How Is It Used?

Form 50 Bis, or the WHT certificate under Section 50 Bis of the Revenue Code, is a document the "payer" must issue to the "payee" every time a withholding is made — as evidence that tax has been deducted and remitted.

In the context of sellers and platforms:

- Form 50 Bis issued by the seller (corporate entity) to the platform — serves as evidence that the seller has withheld tax on platform fees and remitted the full amount to the Revenue Department. The platform uses this to credit its own tax liability.

- If using the agent system: the platform issues Form 50 Bis to itself in the seller's name. The seller does not need to issue it directly, but should retain copies along with the submitted PND53 forms for verification.

Benefits of correct compliance for corporate sellers:

To be clear — the WHT that the seller withholds and remits is a credit belonging to the platform (TikTok Shop / Shopee) as the recipient. It is not a credit for the seller. The seller therefore cannot use that WHT amount as a direct offset against its own corporate income tax liability (PND50).

The benefits for sellers come in two forms:

- The full platform fee is a deductible business expense — the entire fee paid to the platform (both the withheld WHT portion and the amount actually transferred) may be recorded as an expense in calculating net profit, thereby indirectly reducing the corporate tax base.

- Proper expense documentation — Form 50 Bis and the submitted PND53 are documentary evidence that platform fees are genuine business expenses, protecting against the Revenue Department disallowing them during an audit.

For example, if a company pays a total of THB 60,000 in platform fees for the year and THB 1,800 (3%) is withheld as WHT, the deductible expense for net profit calculation is the full THB 60,000 — not just the THB 58,200 actually transferred — which indirectly reduces the company's tax liability.

For more on tax efficiency strategies for business owners, see our article on how business owners can withdraw money from their company using 5 legal methods.

If WHT Has Already Been Remitted, Can the Seller Get a Refund?

No — and this is a common misunderstanding.

The WHT that the seller withholds from platform fees and remits to the Revenue Department is legally a credit belonging to the platform (TikTok Shop / Shopee) as the "recipient." Under WHT law, the party with the right to claim a refund or use this credit is the platform — not the seller.

Form Kor.10 (tax refund request) applies to situations where your own income has had too much WHT withheld against it — a completely different scenario from this article, where the seller is the payer, not the recipient.

When calculation errors may cause problems:

If a seller makes an error in calculating the WHT base — for example, withholding on the VAT-inclusive amount instead of the pre-VAT amount — the correct course of action is to coordinate directly with the platform, so the platform can request an adjustment or refund with respect to its own tax credit. The seller does not file a refund claim directly in this case.

⚠️ Risk: What Happens If You Don't Withhold, or Withhold Incorrectly?

If a corporate entity fails to withhold tax on platform fees as required by law, the following risks apply:

- 1.5% monthly surcharge on the unremitted tax amount, calculated from the due date

- Criminal fine under Section 26 of the Revenue Code

- Platform fees paid without proper WHT may be disallowed by the Revenue Department as deductible expenses in net profit calculations

- Long-term risk: the Revenue Department currently receives transaction data directly from e-commerce platforms, meaning non-compliance is increasingly likely to be detected

If you are unsure whether your business should operate as an individual or a registered company, you can read our Individual vs. Company Business Structure Comparison to help inform your decision.

Summary: What Should You Do?

| Your Situation | Action Required |

|---|---|

| Individual seller on TikTok Shop / Shopee | No WHT obligation on platform fees. File PND90 at year-end. |

| Corporate entity and not yet registered with agent system | Register with Shopee or TikTok Shop's agent system as soon as possible |

| Corporate entity already using the agent system | Review monthly PND53 filings submitted by the platform; compile WHT credits for year-end tax reconciliation |

| Corporate entity that made a WHT calculation error | Coordinate directly with the platform — WHT credit belongs to the platform, not the seller |

WHT compliance with e-commerce platforms may seem complex, but if you are already using the platform's agent system, most of it is handled automatically. The key priority is to compile your WHT credit records every month so you can make the most of them at year-end tax filing.

If you would like the Orbit Advisory team to handle monthly withholding tax and bookkeeping for your online store end-to-end, get in touch with us today.

Frequently Asked Questions

Q1: If I don't appoint the platform as a WHT agent, what steps must a corporate entity handle themselves? A: Corporate entities that don't use the agent system must withhold WHT themselves each time they pay platform fees — 3% on service fees and 1% on logistics. They must file Form PND53 and remit tax to the Revenue Department by the 7th of the following month (or 15th if filing online), and issue Form 50 Bis to the platform as evidence.

Q2: What is the WHT certificate (Form 50 Bis) in this context, and who receives it? A: In this case, the seller (corporate entity) is the payer of platform fees, so the seller must issue Form 50 Bis to the platform as the recipient. Form 50 Bis under Section 50 Bis of the Revenue Code certifies that tax has been withheld and remitted. Sellers should retain a copy to support their annual corporate income tax filing (PND50).

Q3: Do individual sellers on TikTok Shop and Shopee need to withhold tax on platform fees? A: No. Revenue Department Order TP 4/1985 requires WHT on service fees only from corporate entities acting as payers. Individual sellers have no obligation to withhold in this case, but must still report all sales income in their annual personal income tax return (PND90).

Q4: Is the 3% WHT calculated on total sales revenue or on platform fees only? A: It is calculated on platform fees only — not total sales revenue. For example, if monthly sales are THB 100,000 and the platform charges a GP fee of THB 5,000, the 3% WHT applies to THB 5,000 = THB 150 — not to THB 100,000. The WHT amount is therefore a small fraction of total revenue.

Q5: What penalties apply if a corporate entity has not been withholding tax on platform fees? A: Two penalties apply: a 1.5% monthly surcharge on unremitted tax from the due date, plus criminal fines under Section 26 of the Revenue Code. Additionally, platform fees paid without proper WHT deduction may be disallowed as deductible business expenses, resulting in higher corporate income tax liability.

📚 Related Articles

Online Sellers & Freelancers: Should You Register a Company? Clear Comparison of Taxes, Credibility, and Growth

Should online sellers and freelancers register a company in Thailand? This comparison covers tax rates, credibility, costs, and the income threshold that makes it worthwhile.

Online Sellers & Influencers: Which Tax Filing Method? Deep Dive into Income Types 40(2) vs 40(8) and Optimal Expense Deduction Strategies

Online sellers and influencers: is your income Section 40(2) or 40(8)? The answer determines your deduction rate and how much tax you legally pay.

Deep Dive into 8 Types of Income (40(1) – 40(8)): What Type is Your Income and How to Deduct Expenses for Maximum Tax Savings?

Thailand's Revenue Code classifies income into 8 types (Section 40). Your type determines deduction rates — the difference can be tens of thousands of baht.

Swipe to see more →

Ready to Take Action?

Our expert team is ready to help you achieve your financial goals. Contact us through your preferred channel.